Verified Banking and Fast Payment Methods at Non-GamStop Casinos

A UK player who has decided to look at a non-GamStop casino sits inside a payment system that the offshore operator does not control. The operator can publish a list of accepted methods. The UK retail bank, the e-wallet provider and the card networks each independently decide whether any specific transaction goes through. This page documents what works, what does not work, and why, in 2026.

While using credit cards is highly convenient, players must also be aware of the risks and dispute resolution processes associated with offshore transactions.

Table of Contents

- UK Payment Regulations and Offshore Cashier Cashout Processing

- Cards: what really works at offshore casinos

- E-wallets: a clearer ladder

- Cryptocurrency: the rail that bypasses banks

- Bank transfer and Faster Payments

- How licensing shapes payment policy

- Bank-side responsible-gambling tools

- Reading a payment page before depositing

- About the author

UK Payment Regulations and Offshore Cashier Cashout Processing

The starting point is a UKGC rule that does not apply to offshore operators directly but reshapes the payment environment around them anyway. The UK Gambling Commission credit-card ban took effect in 2020 under Licence Condition 6.1.2 of the LCCP, announced in 2020. The ban applies to UKGC-licensed remote operators only; an offshore casino is, by definition, not subject to it.

The interesting consequence is downstream. UK card issuers built compliance and risk infrastructure around the ban. Once the screening was in place, banks extended Merchant Category Code (MCC) 7995 gambling-transaction screening across their card portfolios. The screening fires regardless of whether the merchant on the other side holds a UKGC licence.

For the wider operator-side context behind these rails, see the operator landscape behind these payment rails.

Cards: what really works at offshore casinos

The single most counter-intuitive fact about non-GamStop card payments is this: the casino’s “accepted” list and the UK player’s experience are different things. An offshore casino can accept Visa, Mastercard, Visa Debit, Mastercard Debit, credit and debit alike. The UK-issuing bank is independently deciding whether to authorise each individual transaction.

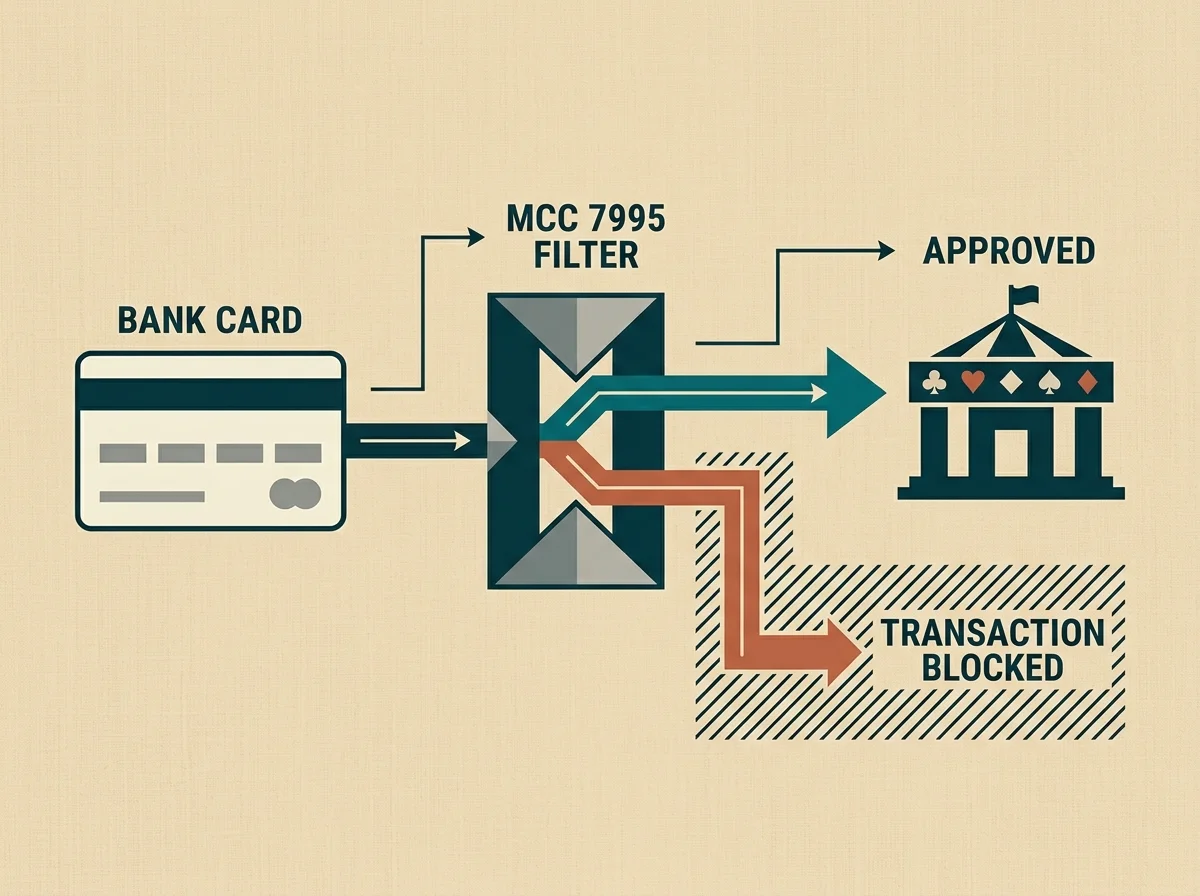

How the MCC 7995 block works

Every transaction sent to a card network carries a Merchant Category Code, a four-digit identifier of the merchant’s industry. MCC 7995 is the code for “Betting (including lottery tickets, casino gaming chips, off-track betting, and wagers at race tracks)”. UK retail banks have built screening rules that flag MCC 7995 transactions for additional review or automatic decline.

Banks that apply gambling-transaction screening or in-app gambling blocks in 2026 include Barclays, HSBC, Lloyds, NatWest, first direct, Halifax, Monzo and Revolut. Implementation varies. Some banks decline MCC 7995 transactions outright when the customer has toggled an in-app gambling block. Others apply softer review with friction (additional 3D Secure prompts, transaction limits, or cooling-off pauses).

What this means in practice

Visa Debit and Mastercard Debit are the most reliably working card types for non-GamStop casinos, but only when the issuing bank has not applied a gambling block. Credit cards on UK-issued accounts are increasingly declined. Apple Pay and Google Pay route through the underlying card networks, so bank-level blocks still apply to them. A transaction declined at the UK bank does not reach the casino’s processor; the casino sees nothing.

The MCC 7995 screening is therefore the single most important variable. A UK player’s first practical question is not “does the casino accept my card” but “does my bank let this transaction through”.

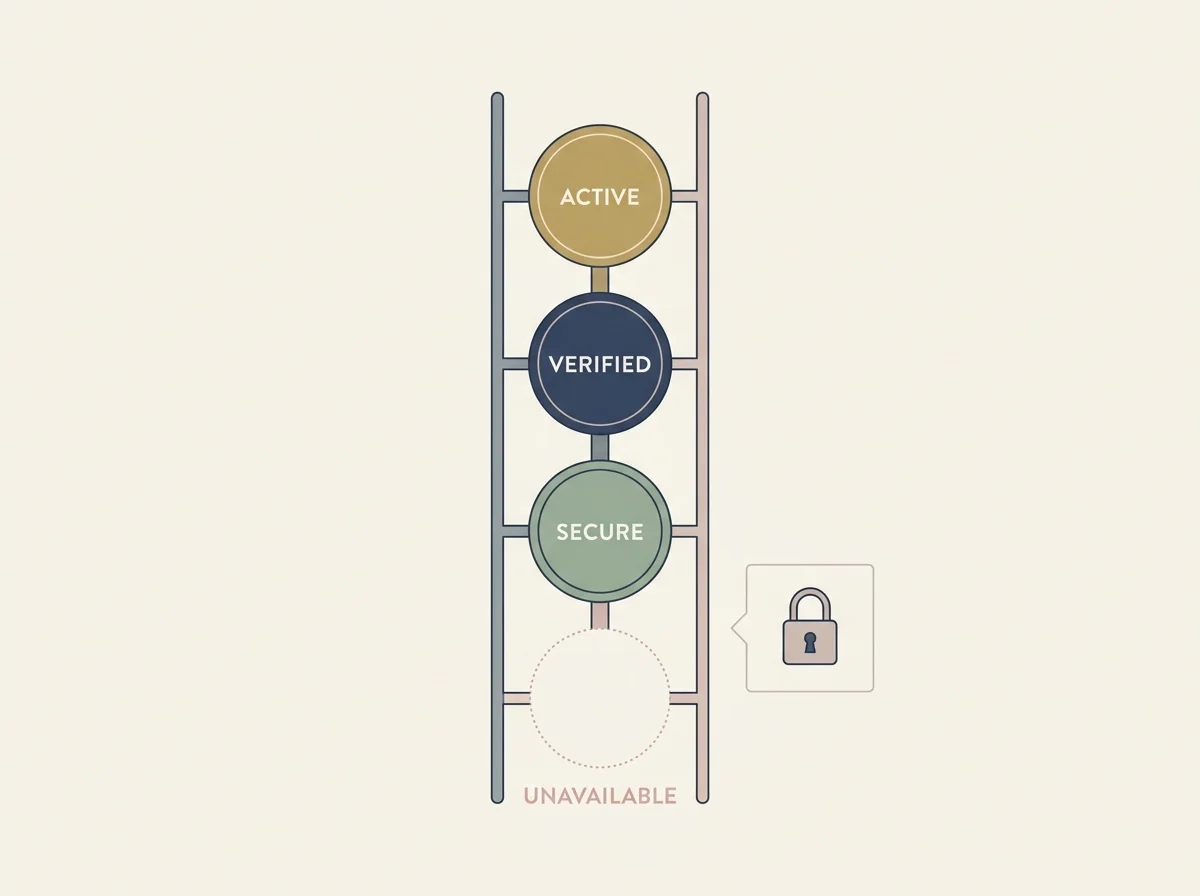

E-wallets: a clearer ladder

E-wallets sit in a different regulatory position. They are licensed payment institutions in their own right and they choose which merchants to onboard. The result is a clearer ladder of what works and what does not.

Skrill, Neteller and ecoPayz

Commonly supported at non-GamStop casinos. Deposits are typically instant. Withdrawals run 24 hours to three days depending on the operator’s processing queue and any KYC checks. These wallets are the workhorse rails of the offshore casino space.

Revolut

Increasingly common as a deposit and withdrawal method. Revolut’s multi-currency accounts soften the foreign-exchange overhead that hits a UK player paying a USD-denominated casino. Revolut also offers an in-app gambling block as a responsible-gambling tool; the block fires before the transaction reaches the casino.

PayPal

Structurally rare at non-GamStop casinos. PayPal restricts merchant onboarding to licensed gambling jurisdictions, which in practice means UKGC, MGA or similarly tier-one authorities. A casino claiming to accept PayPal without a UKGC or MGA licence is either misrepresenting its payment options or operating an unsupported workaround. A UK player should treat PayPal acceptance at a non-GamStop site as a verification trigger before depositing.

Apple Pay and Google Pay

Available at some offshore brands but routed through the underlying card networks. The bank-level MCC 7995 block still applies. Functionally these are card transactions wearing a different user interface.

Cryptocurrency: the rail that bypasses banks

Crypto sits outside the bank-level screening entirely. Most non-GamStop crypto-first casinos accept BTC, ETH, LTC, USDT, USDC, XRP, TRX, SOL and a long tail of altcoins, sometimes 15 to 20 distinct assets.

Deposits are typically instant once the network confirmation requirements are met. Withdrawals are minutes to under an hour, network-dependent. There is no MCC 7995 block because no bank is in the transaction path. There is no UK foreign-exchange overhead because the asset is the same on both ends.

What the crypto rail does not eliminate

Volatility risk on non-stablecoin holdings. A deposit funded in BTC carries the market risk of the underlying asset during the time it sits in the casino balance. Stablecoins (USDT, USDC) remove that risk in normal conditions but introduce counterparty risk on the stablecoin issuer.

KYC triggers are still real. Crypto-first casinos typically apply lighter or no KYC at signup and during routine small-stakes play. They apply KYC at fiat conversion, at large withdrawals, or in flagged regions. JackBit/Jack.com under Ryker B.V. (Curacao OGL/2024/1800/1049) is illustrative: weekly withdrawal caps of around $25,000 with KYC routinely triggered at the upper limits.

And the crypto rail does not restore consumer protection. The deposit is now denominated in a volatile asset, held in a non-UK regulated account, and the player’s recourse is the licensing jurisdiction or a third-party mediator. See the risk profile when withdrawals stall for the dispute side.

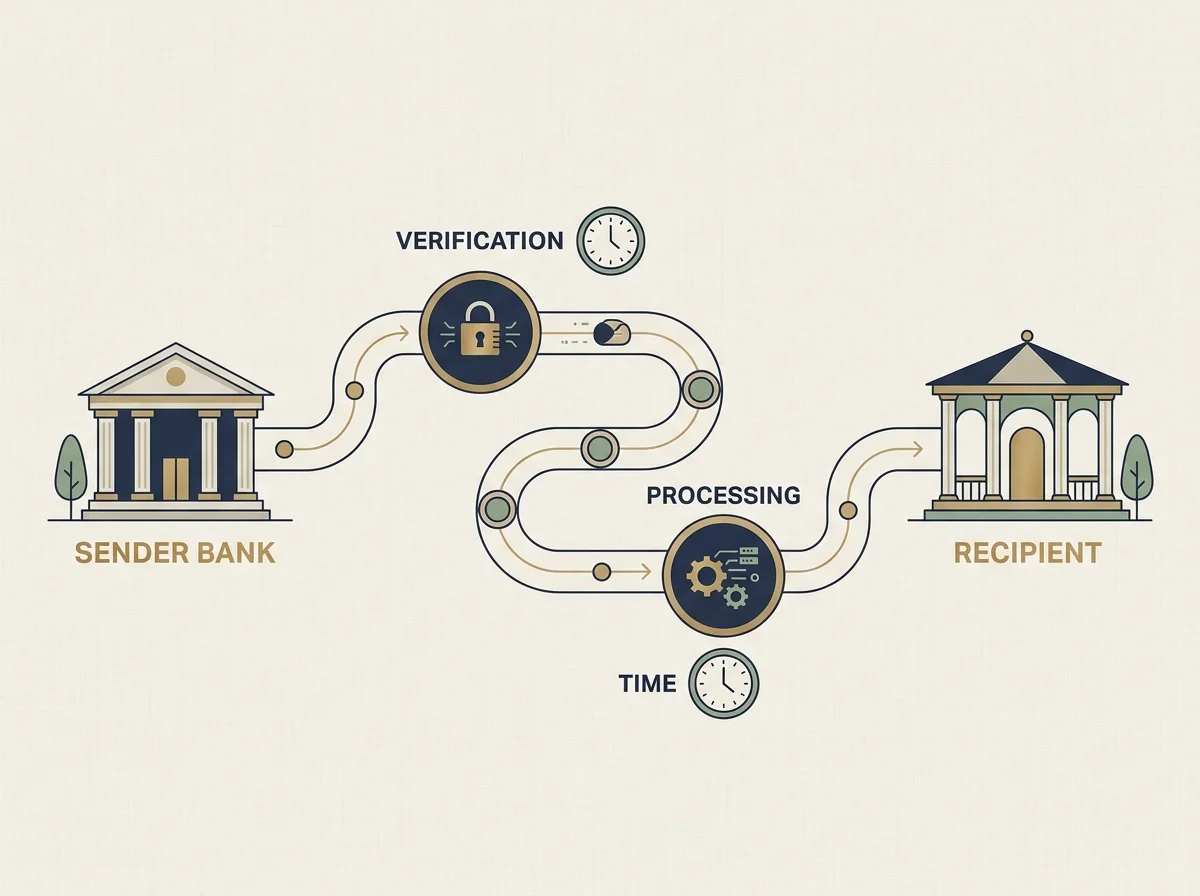

Bank transfer and Faster Payments

Bank transfer is supported at most non-GamStop casinos but slowly. Faster Payments in the UK can reach the casino’s processor in hours; the casino’s internal processing then adds one to five business days depending on operator. Withdrawals via bank transfer tend to be the slowest route, often three to five business days.

Bank transfer also triggers more verification. Higher-value movements draw bank-side anti-money-laundering scrutiny and casino-side enhanced KYC. For a UK player wanting fast withdrawals, bank transfer is structurally the wrong rail. For a UK player wanting an audit trail and the cleanest accounting, it is the right one.

Boku and pay-by-phone

Rare at non-GamStop sites. The carrier billing infrastructure that supports Boku is tied to UK-regulated merchants; offshore casinos are typically not onboarded.

Why processing windows vary so widely

Two factors drive most of the processing-window variance a UK player will see at a non-GamStop casino. The operator’s internal review queue is the first; faster operators settle payouts in hours, slower ones in days. The second factor is the chain of intermediaries between the casino’s processor and the destination account: each hop adds compliance and AML checks. A bank transfer to a UK account hits more checkpoints than a crypto withdrawal to a self-custodial wallet, which is the structural reason for the speed gap.

How licensing shapes payment policy

The casino’s licensing jurisdiction affects which payment rails it can plug into. Curacao OGL-licensed operators have the widest crypto acceptance and reasonable e-wallet coverage. Anjouan-licensed operators are typically crypto-heavy and lighter on card support. MGA-licensed operators look more like UKGC operators in their payment-rail behaviour, with strong card support and minimal crypto presence.

The detail of the licensing comparison sits on Curacao, Anjouan and MGA payment context. The UKGC framework that all of this is contrasted against is documented in the Commission’s guidance and at gov.uk.

Bank-side responsible-gambling tools

The most under-used responsible-gambling tool in the UK in 2026 sits inside the player’s own banking app. Every major UK retail bank now offers a gambling-transaction block that can be toggled in the app. The block applies the MCC 7995 filter to all card transactions and stays in place for a cooling-off period (commonly 48 hours to 7 days) before it can be lifted.

The block is operator-agnostic. It applies to UKGC-licensed sites and offshore sites alike, and it sits at the issuing bank rather than at the casino, so it cannot be bypassed by changing operator. Gamban (device-level block, around £24.99 per year and free via TalkBanStop for those in hardship) sits alongside it as a device-level tool that blocks gambling sites regardless of payment method.

For the wider scheme this all sits outside of, see the GamStop scheme this all sits outside of.

UK support that is free and available now:

- National Gambling Helpline: 0808 8020 133 (free, 24/7, GamCare-run)

- gamcare.org.uk for counselling and treatment

- begambleaware.org for live chat and treatment funding

- gamstop.co.uk for the self-exclusion scheme itself

- NHS National Gambling Treatment Service

- Samaritans: 116 123

Reading a payment page before depositing

A non-GamStop casino’s payment page lists what the casino accepts. It does not list what the player’s bank will allow. The practical reading exercise is to combine three sources.

The casino payment list: what rails the operator is plugged into. The bank’s gambling-transaction policy: what the issuing bank will let through. The Terms and Conditions on processing windows: how long withdrawals actually take and what KYC events the operator can trigger between deposit and payout.

For the full picture across the operator landscape, see the full UK guide to casinos not on GamStop.

About the author

Daniel Ashworth covers UK iGaming regulation, self-exclusion frameworks and the offshore operator landscape that sits outside the Gambling Commission perimeter. With over twelve years analysing licensed and non-UK gambling markets, he writes about the practical impact of tools like GamStop, affordability checks and KYC requirements on British players. His work focuses on how licensing jurisdiction, payment infrastructure and consumer-protection regimes shape the real-world experience of using a casino outside the UK system. He holds certifications in responsible gambling practice and has contributed analysis to research on multi-operator self-exclusion schemes.

Enjoy fast withdrawals and high deposit limits at the top-rated independent casino sites reviewed by our financial experts.