Offshore Non-GamStop Casinos Matrix for Verified UK Operators

When a UK player looks past the GamStop register, they are not looking at a uniform marketplace. They are looking at a fragmented field of operators built around different licences, different operating companies and very different attitudes to KYC, withdrawals and dispute resolution. This page is the operator-side counterpart to the scheme-side material on what GamStop is and how it works. It teaches the reader how to read the landscape, not which casino to pick.

Before registering with a new operator, you should familiarise yourself with the various non-GamStop payment methods to ensure your preferred banking options are supported.

Table of Contents

- Non-GamStop Casino Operational Definitions and Verified Structural Realities

- Categories of operators in the non-GamStop space

- Which licences populate the non-GamStop space

- The 2026 market structure

- Concentration risk: one licence, several consumer brands

- How to verify a licence in under a minute

- Where the market information actually lives

- How money actually moves to and from these operators

- Responsible gambling resources for the UK

- What this means for a UK player in 2026

- About the author

Non-GamStop Casino Operational Definitions and Verified Structural Realities

“Casino not on GamStop” is a definitional shortcut. GamStop is the UK’s national online self-exclusion scheme, run by NOSES (the National Online Self-Exclusion Scheme Limited) since 2018 and mandatory for every UK Gambling Commission (UKGC) licensee since 2020. Integration with GamStop is itself a UKGC licence condition. The logical consequence: any operator absent from the GamStop register is, by definition, an operator that does not hold a UKGC remote licence.

That single fact drives everything else on this page. A non-GamStop casino is an offshore-licensed operator, sitting outside the UKGC’s regulatory perimeter. It may hold a licence from Curacao, Anjouan, Malta or another jurisdiction, or in rare cases none at all. None of those licences require GamStop integration. None of them deliver the UK player-protection framework that a UKGC licence carries.

The licence position determines the legal exposure. Section 33 of the Gambling Act 2005 makes it a summary offence for an operator to provide facilities for gambling in Great Britain without a UKGC operating licence. The offence sits with the operator, not the player. For more on that asymmetry, see Section 33 and the targeting question.

Categories of operators in the non-GamStop space

The non-GamStop space is not a single product category. UK-facing offshore casinos cluster into roughly five operator archetypes, and recognising which one you are looking at changes what risks matter.

Slots-first brands

Built around a lobby of 3,000 to 8,000+ slot titles aggregated from 50-100 studios (Pragmatic Play, Play’n GO, NetEnt, Red Tiger, Hacksaw, Blueprint and so on). Bonuses are aggressive, often 200-600% across multi-tier welcome packages. The economic centre is wagering volume, and the operating company is typically Curacao-incorporated.

Live-casino-first brands

Lean heavily on Evolution Gaming, Pragmatic Play Live and Ezugi, with hundreds of live tables and game-show titles (Crazy Time, Monopoly Big Baller, Mega Wheel). Wagering caps and table limits are typically higher than at UKGC sites; bonus integration with live play is restricted.

Crypto-first platforms

These accept BTC, ETH, USDT, USDC, LTC, XRP and a long tail of altcoins, often as the default deposit method. Many pair the casino with an integrated sportsbook. KYC is typically lighter for crypto-only play; fiat use triggers stricter checks. JackBit, which rebranded to Jack.com in mid-2026, sits in this archetype: operated by Ryker B.V., Curacao licence OGL/2024/1800/1049, with weekly withdrawal caps of around $25,000.

Sportsbook-led brands with a casino vertical

Sports is the front door; casino and live casino sit behind it. Withdrawal speeds and bonus economics follow sportsbook conventions (lower wagering, lower max bet caps) rather than slot-led ones. The same Curacao or Anjouan licensing pattern applies.

Small affiliate-tied brands

The riskiest category. Short brand history, opaque operating company, and a website-template feel shared across a dozen near-identical sites. The operating company on the licence certificate often does not match the company name in the footer Terms and Conditions; sometimes the underlying entity shifts between review cycles. Treat any brand fitting this profile as a stranger you have not yet identified.

Which licences populate the non-GamStop space

A high-level view here; the detailed comparison lives on the licensing-jurisdictions breakdown in detail. Five jurisdictions dominate the operator pool serving UK players in 2026.

Curacao under the 2024 OGL framework

By far the most common. The 2024 reform under the National Ordinance on Games of Chance (LOK 2023) consolidated the old master-licence / sub-licence model into a single regulator: the Curacao Gaming Authority (operationally branded Gaming Control Board). New licences are issued in the OGL/YYYY/NNNN/MMMM format, replacing the legacy 1668/JAZ, 5536/JAZ, 8048/JAZ and 365/JAZ master-licence numbers.

Anjouan (Union of Comoros)

Licences issued by the Government of the Autonomous Island of Anjouan in the ALSI-NNNNNNNN-FXX format. Cheaper than Curacao, with roughly 4-week issuance and a lighter regulatory disclosure regime.

Kahnawake (Mohawk Territory, Canada)

An older offshore jurisdiction, increasingly rare for UK-facing brands in 2026. Strong on operational discipline by historical reputation but a small share of the modern non-GamStop pool.

Costa Rica

Not a true gambling licence. Operators register as data-processing businesses; there is no specific gambling regulator and no gambling-specific oversight. Treated by mainstream review sites as the weakest credential.

Malta Gaming Authority (MGA)

Strong player-protection regime: fund segregation, anti-fraud monitoring, formal complaints handling. A UK player will rarely find an MGA-licensed non-GamStop casino because most MGA operators that take UK customers also hold a UKGC licence and are therefore on GamStop.

The 2026 market structure

The non-GamStop pool is contested territory in regulatory terms. Industry research commissioned by the Betting and Gaming Council and prepared by H2 Gambling Capital estimates UK offshore stakes rose from approximately £5 billion in 2019 to £16.6 billion in 2025, with legal-market share falling from 97% to 92% over the same period. The UK Gambling Commission has explicitly declined to endorse those numbers and has questioned the methodology, while pursuing its own research into the size and drivers of the unlicensed market.

Independent research (Yield Sec, 2025) put the number of illegal sports betting and casino operators actively targeting the UK at more than 500, with over 1,100 affiliates promoting them. The Commission’s 2026-27 business plan scales up enforcement: 741 cease-and-desist notices in the recent enforcement programme, more than 1,000 referrals of website URLs to search engines for delisting, and around 1,100 websites geo-blocked or removed in the period leading up to 2026. Treasury allocated an additional £26 million over three years for illegal-markets enforcement, and the Commission has been recruiting a new “Head of Illegal Markets” role in 2026.

Two large consequences for UK players. First, the search-engine and payment-processor disruption is real; UK-issued cards and search results increasingly route around offshore brands. Second, several high-profile crypto brands that previously accepted UK customers no longer do.

Brand departures and UK access restrictions

Stake.com operated in the UK via TGP Europe (UKGC operating licence number 39368) until 2025, when it surrendered the UK licence following an Advertising Standards Authority investigation and a £3.3 million UKGC penalty against TGP Europe. As of 2026, Stake.com geo-blocks UK IP addresses. TGP Europe had earlier received a £316,250 penalty in 2023 for anti-money-laundering and social-responsibility failures.

BC.Game (operator Twocent Technology Ltd., Anjouan licence ALSI-202410011-FI1) explicitly restricts the United Kingdom in its terms. Lucky Block (operator Entretenimiento Rojo B.V., Curacao) restricts the United Kingdom alongside the United States, Australia, France, the Netherlands, Spain and Italy. Treat any 2024-dated or older affiliate listicle that recommends these three brands to UK players as out of date.

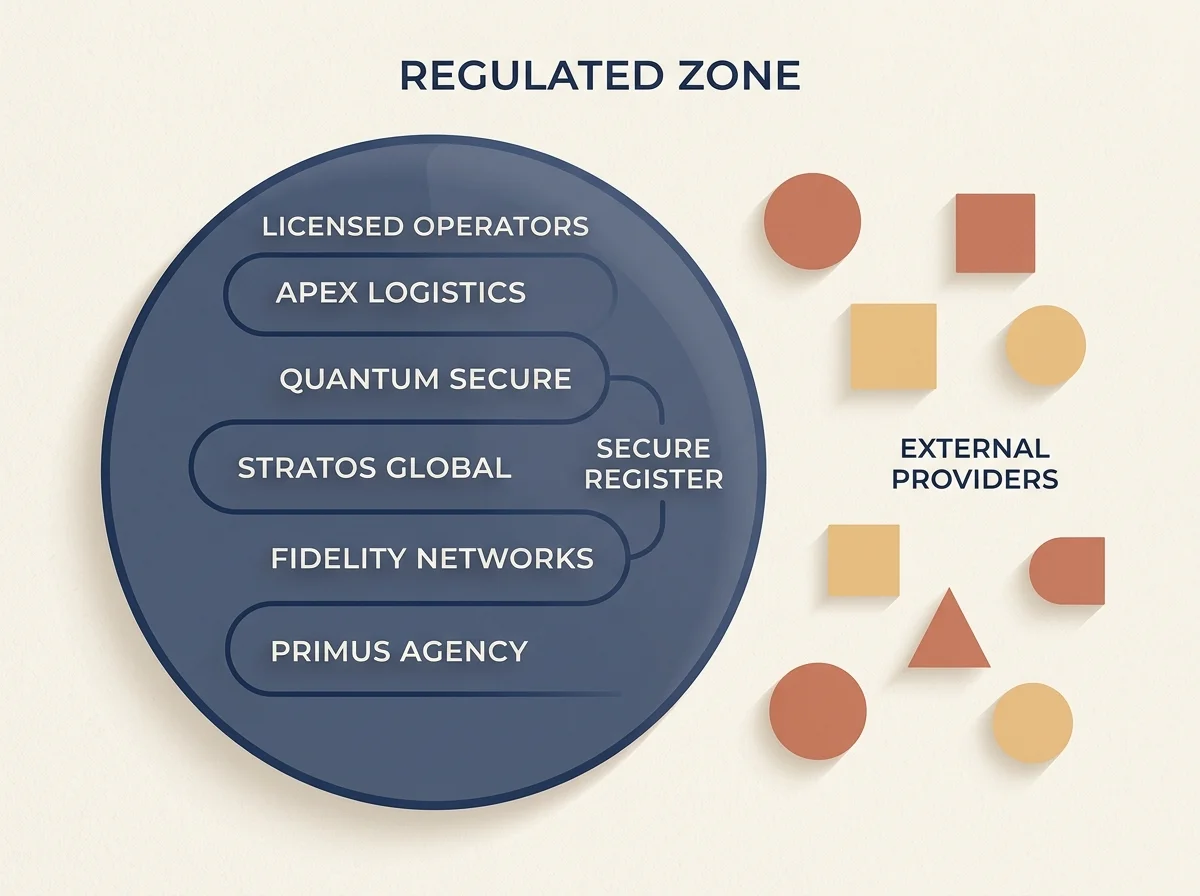

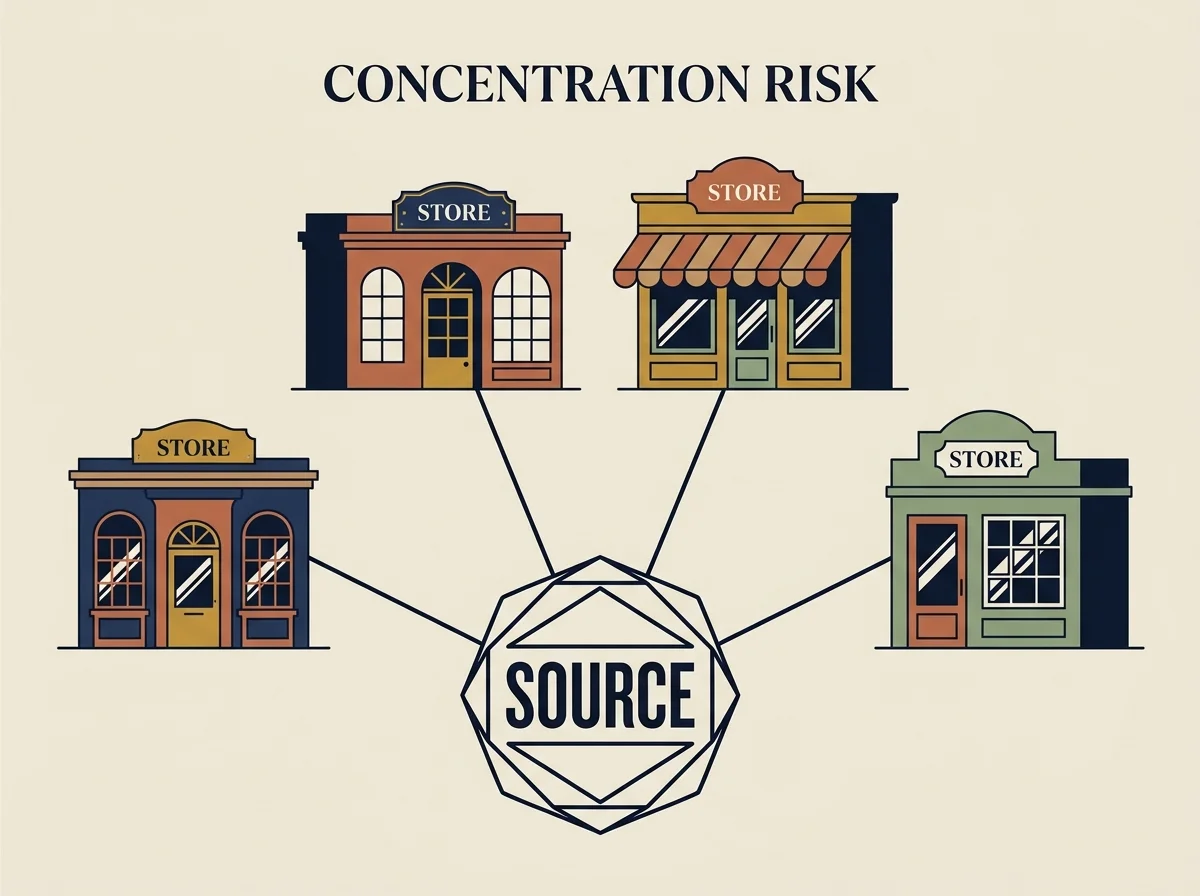

Concentration risk: one licence, several consumer brands

One of the most under-discussed features of the non-GamStop market is that “several different casinos” often turn out to be a single operating company running multiple consumer-facing skins under one Curacao licence. The economics make sense for the operator (one infrastructure, several brand campaigns, several SEO and affiliate footprints). The implication for the player is less obvious.

A live worked example: Santeda International B.V. (Curacao company number 151296, registered at Zuikertuintjeweg Z/N, Curacao) holds Curacao Gaming Control Board licence OGL/2024/1798/1048. The same operating company and the same licence number sit behind several consumer-facing casino brands, including MyStake, Goldenbet, Rolletto and others in the same family. Affiliate review sites describe the network as a single Santeda group; an industry report in early 2026 attributed material wagering volume on behalf of British customers to that single network.

The risk-marker is structural. If a UK player has a dispute with one Santeda brand, they are not negotiating with a single consumer-facing brand: they are negotiating with the same legal counterparty that controls the other brands. A blanket account-closure or balance-forfeiture decision can apply across the network. And a brand-level “switch” to a sister site does not represent an independent regulatory counterparty.

Concentration risk is not unique to Santeda. Other operating companies (Ryker B.V. for JackBit/Jack.com, Group Gaem B.V. for Winstler, and several smaller groups) follow similar patterns. The lesson for the player is to identify the operating company on every casino’s footer before treating two brand names as two independent options.

How to verify a licence in under a minute

Operator footers are not regulators. A licence logo or a static image is not verification; it is decoration. The verification step the player needs to do is brief but mandatory.

- Find the operating company name on the footer. The legal entity should be named in full, with a Curacao company number or equivalent, plus the registered address.

- Find the licence number. Curacao OGL licences carry the OGL/YYYY/NNNN/MMMM format; Anjouan licences carry the ALSI- prefix.

- Open the regulator’s public register in a separate tab. The Curacao Gaming Control Board verification portal returns the same operating company, the same licence number and a status of “Active” or otherwise.

- Cross-check the registered company name. The legal entity on the casino footer must match the entity on the regulator’s register. A mismatch is a red flag.

- Compare against the casino’s Terms and Conditions. The contracting party named there should be the same operating company.

Clone-site fraud is a real category. A scam operator builds a near-identical website on a look-alike domain, copies the trade dress of an established brand and references a licence number that the cloned brand actually holds. A 30-second register check exposes the clone every time. The player who does not check is the player who finds their deposit gone.

Where the market information actually lives

For non-GamStop operators there is no equivalent of the UKGC public register, no equivalent of IBAS (the UKGC-approved Alternative Dispute Resolution body) and no equivalent of the Financial Ombudsman Service. The information the player has to rely on is fragmented across three layers.

First, the regulator’s register. Curacao GCB and the Anjouan Gaming Authority each maintain a register that confirms the licence and the operating company, but neither runs a complaint-handling service the player can use as enforcement leverage.

Second, third-party complaint mediators. Casino Guru, AskGamblers AGCCS (the AskGamblers Casino Complaint Service) and a handful of smaller services operate as informal mediators. They publish dispute outcomes and apply reputational pressure on operators. They have no statutory enforcement power. Their leverage is the operator’s willingness to protect its brand image and affiliate-channel placement.

Third, affiliate review sites. The bulk of UK SERP results for non-GamStop terms are affiliate listicles. These describe operators, but they are not neutral and they cannot enforce anything. They are useful for identifying the operating company and the licence number; they are not useful as a substitute for a regulator.

The structural protection gap is not theoretical. The detail lives on the structural risk profile beyond UKGC, including specific patterns observed in account closures and withdrawal delays.

How money actually moves to and from these operators

Payment infrastructure shapes the experience far more than the marketing pitch suggests. The UKGC credit-card ban under the Gambling Act 2005 framework applies to UKGC operators only; it does not bind offshore operators directly. What does bite is the issuing bank. Every major UK retail bank applies Merchant Category Code (MCC) 7995 gambling-transaction screening at the card-issuing level, and these blocks fire regardless of whether the casino itself is UKGC-licensed.

The result is a counter-intuitive sequence. A UK player tries a Visa credit card at an offshore casino; the casino “accepts” credit cards under its own terms; the player’s UK-issuing bank declines the transaction before it reaches the casino’s processor. The same logic applies to Apple Pay and Google Pay, which route through the underlying card networks.

E-wallets follow a clearer ladder. Skrill, Neteller and ecoPayz are commonly supported and settle quickly. Revolut works but exposes the user to Revolut’s own in-app gambling block. PayPal is structurally rare because PayPal restricts merchant onboarding to licensed jurisdictions. Crypto sits outside the bank block entirely and is the most reliable route for crypto-fluent users, with deposits often instant and withdrawals minutes to under an hour, balanced against volatility on non-stablecoin holdings.

The full breakdown lives on cards, e-wallets and crypto at offshore casinos.

Responsible gambling resources for the UK

A player who is reading the non-GamStop landscape because they are already self-excluded should pause before going further. The reason they registered with GamStop is the same reason offshore operators are a higher-risk environment for them specifically. UK support is available now, free, and confidential.

- National Gambling Helpline: 0808 8020 133 (free, 24/7, run by GamCare)

- BeGambleAware: begambleaware.org (live chat, treatment funding)

- GamCare: gamcare.org.uk (counselling, treatment, self-help tools)

- GAMSTOP: gamstop.co.uk (the scheme itself)

- NHS National Gambling Treatment Service: nhs.uk (specialist NHS clinics)

- Samaritans (general emotional distress): 116 123

If a self-exclusion has expired and you want to be removed from the register, the route is a phone call to 0800 138 6518 followed by a mandatory 24-hour cooling-off period. That route is documented on the page covering the GamStop expiry process.

What this means for a UK player in 2026

Reading the non-GamStop landscape is not the same as endorsing it. The five operator archetypes, the five licensing jurisdictions, the concentration-risk pattern and the payment-rail mechanics all sit underneath a single fact: this is the market the UKGC perimeter excludes. Everything missing from a UKGC licensee (GamStop coverage, IBAS dispute access, affordability checks, stake caps, mandatory KYC discipline, mandatory responsible-gambling tooling) is missing for a reason, and at an offshore casino the player chooses to take that gap on themselves.

The practical reading lesson is the operating company, the licence number, the regulator’s register entry, the payment-rail behaviour and the mediator history. None of those substitute for a UKGC licence. They are the minimum the player needs to know who is on the other side of the screen.

For the full pyramid in one document, see the full UK guide to casinos not on GamStop. For the operator-side detail, the three supporting pages in this cluster cover the licence regimes, the payment infrastructure and the structural risk profile in turn.

About the author

Daniel Ashworth covers UK iGaming regulation, self-exclusion frameworks and the offshore operator landscape that sits outside the Gambling Commission perimeter. With over twelve years analysing licensed and non-UK gambling markets, he writes about the practical impact of tools like GamStop, affordability checks and KYC requirements on British players. His work focuses on how licensing jurisdiction, payment infrastructure and consumer-protection regimes shape the real-world experience of using a casino outside the UK system. He holds certifications in responsible gambling practice and has contributed analysis to research on multi-operator self-exclusion schemes.

For a thoroughly vetted selection of secure platforms, check out our updated list of the best casinos not on GamStop available to UK players.